How to Fund Legal Fees (Without Destroying Your Financial Future)

Once legal fees start building, most people hit the same wall: “How am I actually going to pay for this?”

Once legal fees start building, most people hit the same wall: “How am I actually going to pay for this?”

Going to court is one of the most stressful experiences a person can face. But here’s the part that catches most people

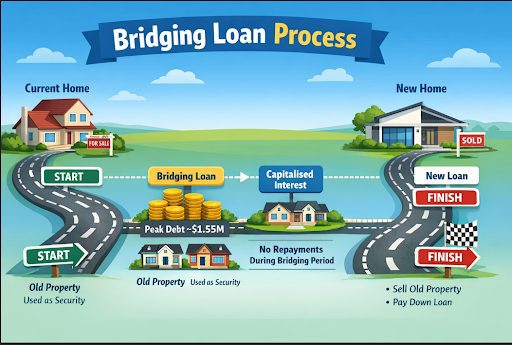

Before diving into why banks have stepped away from bridging finance, it’s worth first understanding what a bridging loan actually