How to Fund Legal Fees (Without Destroying Your Financial Future)

Once legal fees start building, most people hit the same wall: “How am I actually going to pay for this?”

If your goal is being financially free – owning your own house outright, not having to work, and living off passive income that you don’t have to work for – then property can be an excellent method of achieving this goal.

Many people go into property and property investing without a financial goal in mind. They simply haven’t got a firm idea of where they want to end up financially. Creating a financial goal from the outset is perhaps the most important step.

There are many different strategies when investing in property and so many different ways that you can invest; buy and hold, invest in cash-flow, invest in growth, renovate, subdivide, develop, or flip houses, among others.

There are very few people who actually follow through and achieve financial independence. This is where Australian Mortgage Corporation comes in. We can help you along every step to achieve your property goals.

It’s easy to think you have lots of equity, but will the loan be serviced? Find out how much you can borrow with our calculator.

It’s easy to think you have lots of equity, but will the loan be serviced? Find out how much you can borrow with our calculator.

The most traditional way to source a property is through a Real Estate Agent.

Their commission is included in the price. Hence, as a buyer, you are paying this fee. Nowadays, most people will go online to do some preliminary research on availability and price. This is usually followed up by going along to open houses or auctions to try and compete against other (mostly unseen) buyers.

Bear in mind that many times the property is advertised online because it cannot be sold through to Buyer’s Agents, professional investors, or pre-qualified motivated buyers.

This is very much the “Sunday Driver” approach to property investment. It gives you an inaccurate picture of the quality of investment stock, the area, or comparable properties elsewhere. Other key metrics, like demographics, that serious investors track, are also usually absent. As an investor you ought to look for as much information about where you are buying, as what it is that you are buying.

For second-hand properties Buyer’s Agents can be worth their weight in gold.

Buyer’s agents are like Real Estate Agents, only that instead of representing the Vendor, such as Real Estate Agents are legally obliged to do, they represent you, the Buyer. A good Buyer’s Agent will personally specialise in about three or four suburbs only and will secure for you value based property before it hits the market for general sale.

They should be extremely knowledgeable about particular suburbs, prices, planning issues and potential growth. A Buyer’s Agent negotiates a purchase on your behalf and ensures that you never overpay for a property. Their standard fee is 2%. For the right ones, this is more than recouped by how much work and hassle they save you, as well as what you don’t overpay on a purchase price.

Often called Economic Research Houses, these are professionals who specialise in new property on behalf of serious buyers.

They work on your behalf and deal directly with developers to secure you premium properties from quality developers. Quality stock and return on customer’s investment are paramount for Research Houses. The best ones do not charge you, the Buyer, anything for their service. They charge a fee to the developer. They have a long-term view for the investor’s growing portfolio and depend on future opportunities to invest with them in the future.

Research Houses usually have entire departments dedicated to researching property and picking particular projects for clients that will deliver value, growth and rental stability over longer periods.

The most traditional way to source a property is through a Real Estate Agent.

Their commission is included in the price. Hence, as a buyer, you are paying this fee. Nowadays, most people will go online to do some preliminary research on availability and price. This is usually followed up by going along to open houses or auctions to try and compete against other (mostly unseen) buyers.

Bear in mind that many times the property is advertised online because it cannot be sold through to Buyer’s Agents, professional investors, or pre-qualified motivated buyers.

This is very much the “Sunday Driver” approach to property investment. It gives you an inaccurate picture of the quality of investment stock, the area, or comparable properties elsewhere. Other key metrics, like demographics, that serious investors track, are also usually absent. As an investor you ought to look for as much information about where you are buying, as what it is that you are buying.

For second-hand properties Buyer’s Agents can be worth their weight in gold.

Buyer’s agents are like Real Estate Agents, only that instead of representing the Vendor, such as Real Estate Agents are legally obliged to do, they represent you, the Buyer. A good Buyer’s Agent will personally specialise in about three or four suburbs only and will secure for you value based property before it hits the market for general sale.

They should be extremely knowledgeable about particular suburbs, prices, planning issues and potential growth. A Buyer’s Agent negotiates a purchase on your behalf and ensures that you never overpay for a property. Their standard fee is 2%. For the right ones, this is more than recouped by how much work and hassle they save you, as well as what you don’t overpay on a purchase price.

Often called Economic Research Houses, these are professionals who specialise in new property on behalf of serious buyers.

They work on your behalf and deal directly with developers to secure you premium properties from quality developers. Quality stock and return on customer’s investment are paramount for Research Houses. The best ones do not charge you, the Buyer, anything for their service. They charge a fee to the developer. They have a long-term view for the investor’s growing portfolio and depend on future opportunities to invest with them in the future.

Research Houses usually have entire departments dedicated to researching property and picking particular projects for clients that will deliver value, growth and rental stability over longer periods.

For most Australians their goal in life has been to pay off their own home loan as quickly as possible, and only then start looking at investing in property. As property prices increase, this becomes harder and harder and the goal of buying an investment property gets further and further away.

The requirement to cobble together a 20% deposit for a property, and also enough cash to afford stamp duty, means that many have already unnecessarily written off their chances of financial independence before they have even started. However, by securing the right advice and agreeing a strategy, an investment property may be possible much sooner than you think.

There are various tax benefits associated with investment property that many people forgo. This is even true of people who have already invested in property.

In addition, existing homeowners may be able to use equity (the difference between what their home is worth and what they owe) to cover the deposit on an investment property.

Even with very little equity, it is still possible to secure a property.

For most Australians their goal in life has been to pay off their own home loan as quickly as possible, and only then start looking at investing in property. As property prices increase, this becomes harder and harder and the goal of buying an investment property gets further and further away.

The requirement to cobble together a 20% deposit for a property, and also enough cash to afford stamp duty, means that many have already unnecessarily written off their chances of financial independence before they have even started. However, by securing the right advice and agreeing a strategy, an investment property may be possible much sooner than you think.

There are various tax benefits associated with investment property that many people forgo. This is even true of people who have already invested in property.

In addition, existing homeowners may be able to use equity (the difference between what their home is worth and what they owe) to cover the deposit on an investment property.

Even with very little equity, it is still possible to secure a property.

Australia is blessed in that it is not one just big metropolitan property market with a ripple effect across the country.

Australia could be said to be comprised of several different property markets with each having notably distinct characteristics. Perth, Adelaide, and Brisbane might as well be different countries when comparing property prices.

This interesting dynamic itself offers a plurality of options and opportunities to invest. Many property investors have already begun diversifying their holdings.

This is not only to limit their risk of single city exposure, but also as a means of capitalising on growth in other cities such as Sydney, Melbourne, Brisbane and, most recently, Perth.

If you are thinking about investing, we can help you to find the most suitable home loan for an investment property. We will get you a mortgage that best suits your tax efficiency, investment needs and wealth creation goals.

Our aim in Australian Mortgage Corporation is to have you as a long-term client, and so we will go through all of the different scenarios with you and advise you on the product best suited to your needs and ambitions.

When financing your investment property, it’s easy to get lost while navigating all the different types of mortgage loans available and changes that have recently occurred.

You can’t have failed to notice that over the last 18 months your rate has risen anywhere between 0.90% and 1.50%. This means that based on a $750,000 loan you may now be paying over $11,000 per year extra.

However, this doesn’t mean that there aren’t good offers to be found. If you think an investment loan at below 4% is impossible, you haven’t spoken to right people.

Ensuring your loans are structured to maximize tax benefit, as well as cash flow, is something that almost everyone should do, but hardly anyone ever does.

This is not your accountant’s job, so the responsibility falls onto your broker or bank. However, bank staff are rarely, if ever, qualified to discuss this. What’s worse is that they are only interested in getting the loan done quickly, so you usually end up missing out.

Have you looked at “Debt Recycling”? Have you explored the benefits of a Line of Credit? Have you used LMI for tax benefits?

This is an automatic part of our service to you. All these options are explored for your benefit. We can also help you source suitable investment properties to remove the stress of the process.

Do you have equity in your property but can’t get the cash out quickly enough? Mortgages can take weeks or months, by which time the property you want to bid on has already gone.

A Deposit Bond might be exactly the thing for you. This acts like the cash in your property to secure the 10% deposit. It can be done in 24 hours, is extremely cost effective and means you can go to the auction, bid on the house, or buy off the plan, without the stress of remortgaging, proving your income, release of deeds and any of the other hassle.

If you are thinking about investing, we can help you to find the most suitable home loan for an investment property. We will get you a mortgage that best suits your tax efficiency, investment needs and wealth creation goals.

Our aim in Australian Mortgage Corporation is to have you as a long-term client, and so we will go through all of the different scenarios with you and advise you on the product best suited to your needs and ambitions.

When financing your investment property, it’s easy to get lost while navigating all the different types of mortgage loans available and changes that have recently occurred.

You can’t have failed to notice that over the last 18 months your rate has risen anywhere between 0.90% and 1.50%. This means that based on a $750,000 loan you may now be paying over $11,000 per year extra.

However, this doesn’t mean that there aren’t good offers to be found. If you think an investment loan at below 4% is impossible, you haven’t spoken to right people.

Ensuring your loans are structured to maximize tax benefit, as well as cash flow, is something that almost everyone should do, but hardly anyone ever does.

This is not your accountant’s job, so the responsibility falls onto your broker or bank. However, bank staff are rarely, if ever, qualified to discuss this. What’s worse is that they are only interested in getting the loan done quickly, so you usually end up missing out.

Have you looked at “Debt Recycling”? Have you explored the benefits of a Line of Credit? Have you used LMI for tax benefits?

This is an automatic part of our service to you. All these options are explored for your benefit. We can also help you source suitable investment properties to remove the stress of the process.

Do you have equity in your property but can’t get the cash out quickly enough? Mortgages can take weeks or months, by which time the property you want to bid on has already gone.

A Deposit Bond might be exactly the thing for you. This acts like the cash in your property to secure the 10% deposit. It can be done in 24 hours, is extremely cost effective and means you can go to the auction, bid on the house, or buy off the plan, without the stress of remortgaging, proving your income, release of deeds and any of the other hassle.

Annie is an occupational therapist with no dependents. She has a $450,000 mortgage on her home and only 15 years left before she calculates she can retire.

The problem is that her mortgage is due to continue for another 23 years, i.e. 8 years into retirement. Her Super balance is low due to many years of working overseas and self-employed. She basically feels that she can’t afford to retire early.

Through a low-risk, diversified property investment strategy, she has amassed just over $300,000 in equity after just 3 years in investment property. Each property has been cash-flow positive and hence hasn’t required any ‘out-of-pocket’ ongoing expenses.

She is now hopeful of retiring in 5 years, paying off her home loan in full and continuing to invest in property.

Annie is an occupational therapist with no dependents. She has a $450,000 mortgage on her home and only 15 years left before she calculates she can retire.

The problem is that her mortgage is due to continue for another 23 years, i.e. 8 years into retirement. Her Super balance is low due to many years of working overseas and self-employed. She basically feels that she can’t afford to retire early.

Through a low-risk, diversified property investment strategy, she has amassed just over $300,000 in equity after just 3 years in investment property. Each property has been cash-flow positive and hence hasn’t required any ‘out-of-pocket’ ongoing expenses.

She is now hopeful of retiring in 5 years, paying off her home loan in full and continuing to invest in property.

Once legal fees start building, most people hit the same wall: “How am I actually going to pay for this?”

Going to court is one of the most stressful experiences a person can face. But here’s the part that catches most people

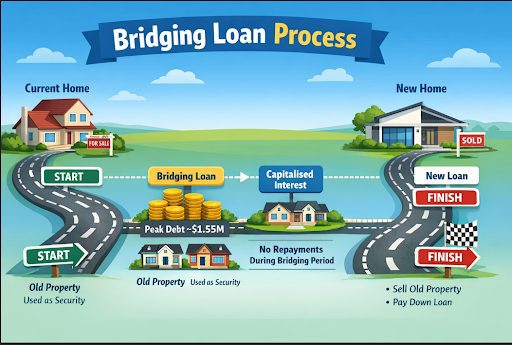

Before diving into why banks have stepped away from bridging finance, it’s worth first understanding what a bridging loan actually