What is a bridging loan?

A bridging loan is a type of short-term financing, typically for the purpose of buying a house before another is sold. The loan usually last anywhere between 2 weeks to 3 years pending the sale or the arrangement of longer-term financing. Typically they are used in one of the following 2 scenarios:

- A person is looking to buy their next home, and sell their existing home; however the settlement date of the purchase happens before the sale goes through of the existing property. (see below table for a worked example of this).

This is the most common scenario and will usually require a normal residential mortgage bridging loan. Recently we have been receiving a higher than usual volume of calls precisely related to this finance.

- Investor or property developer: Requires financing to complete a project, say on a block of units (apartments), and does not have enough pre-sales or financing from a bank. In this case the developer will require finance from a third-party lender to cover the finishing/ construction costs of the project to ready the building in time to sell the complete units directly to the public.

These are typically short-term loans and vary from 6 months to 2 years.

For the purposes of this article, I will deal mainly with the most common type in Australia, which is the residential birding loan. I.e. you are about to buy a next property (can be second-hand) but haven’t gotten your existing one sold yet.

There is much confusion about how these loans work. Regretfully this is needless. It is far simpler than many of them let on. Furthermore, there are quite frequently more options than many mortgage professionals and bankers will want to admit.

Classic bridging loan

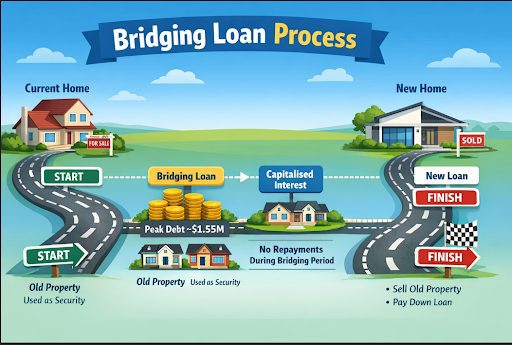

What happens in essence is that the bank takes a legal charge (mortgage) over two properties until such time as you sell the first one. That’s it. It’s as simple as that.

The bank allow you carry both mortgages, which allows you get your ideal home, before you have finalised the sale of your existing home. This is because it’s unreasonable to assume that everyone’s ideal property is available for settlement at exactly the same time as the next owners of your property move in.

See the table below for a worked example:

| Existing home | Next home to be purchased | |

| Value: $1m | Value: $700k | |

| Date of settlement: no buyer yet secured | Date of settlement: 8 weeks away | |

| Value: $1,000,000 | Value / purchase price: $700,000 | |

| Existing mortgage: $200,000 | Cash deposit paid on new property: $35,000 | |

| Total debt needed: $200,000 (existing mortgage)$700,000 (purchase price)$35,000 (est. Stamp Duty & legals)$70,000 (est. renovation costs in new home) $1,005,000 Total cash needed for purchase (Less): ($35,000 [deposit paid]) $970,000 – total finance needed (peak debt) | ||

| Peak debt | The maximum debt carried during the period where you temporarily own 2 properties | |

| $970,000 | Peak debt | |

| 9% | Rate during bridging finance period | |

| 6.39% | Normal P&I mortgage rate for owner occupier | |

| Interest Only | Repayment method during peak debt period | |

| 2 years | Standard maximum bridging period | |

| Interest Only | Repayment method during peak debt period | |

| Maximum LVR | The maximum debt as a proportion to the value of both properties is usually around 70%. | |

There are a few terms that are bandied around that are worth becoming familiar with:

- “Entry-debt”: This refers to the existing debt you have on your property.

- “Peak-debt”: This refers to the total debt of the new property PLUS the exiting mortgage on your existing property.

- “End-debt”: This refers to the debt (mortgage debt) remaining after the sale of the existing property has settled.

- Length of bridging: This refers to the maximum term allowed by the bank to sell your existing property, after having completed on the purchase of the new property. The usual period is between 6 months and 2 years, with 2 years being the most common limit.

- Repayment: Typically all repayments are interest only during the peak-debt period.

- Interest rate: The interest rate is typically more during the peak debt period, usuauly about 2.5% more. SO if a normal mortgage rate was say 6.49% P&I (Owner occupied), the Bridding Laon rate would be approx. 8.99% during the peak debt period (max 2 years).

- Variable or fixed: Most bridging loans are only allowed on variable rates only. This has the benefit of being able to be paid out early without any break fees or charges.

- Loan structure after bridging: After bridging finance elapses, the “end-debt” usually reverts to a P&I repayment over the remaining term. So, if for example, a birding loan was required for only 12 months on a new 30 year mortgage, owner occupied, the end-debt loan would revert to a P&I loan over 29 years. At this stage you can choose to remain variable or take a fixed rate option, if available.

- Can I do bridging finance for a construction / home build? Yes. Surprisingly these are very common. The usual period is 2 years for maximum/ peak debt.

- Early repayment options: Yes. Every lender allows early repayment of a bridging loan. There are no additional fees and charges for paying this down early.

- Does the loan have to be re-underwritten (re-assed by Credit) after bridging period? No, once the biding loan is approved and drawn down, it is not subject to underwriting for as second time.

Things to be aware of:

- Very few banks still do bridging finance.

“Surely not? I’ve been with ACME Bank for years and they told me they do it!”

Simply put no. If it didn’t work for Wile E Cayote, it will not work for you. ACME Bank may be referring to another way around the bridging problem. Given that your end-debt loan is likely to be small or non-existent, not many banks are willing to accommodate a bridging finance request as it simply is not profitable for them to do so. There are a now a small number of banks that offer this. However, those that do vary in terms of quality and efficiency. Some range from the “why do you bother?” to the “I cannot believe it was so easy”. So the option is still there, but the main high street banks have already started pulling out of this market over the last few years.

- There’s always another way.

There are other ways (and sometimes cheaper alternatives) to bridging finance.

Given how it can be tricky to get a bridging finance approved, there are other methods of getting the loan approved, including split loans of Investment and Owner-Occupied properties during the peak debt period. A good broker will go through this with you.

- Caveat loans and bridging finance – red flags

Be wary of google search “Bridging loans brokers”. On a simple Google search and about 70% of what shows up on page 1 will be ads from people pretending to be independent brokers but actually representing caveat lenders. The question is – Are they really brokers? There are many people who are fronts for caveat lenders that pretend to be brokers.

By law, licensed finance brokers must act in your best interest. The law is even called “Best Interests Duty” (Warning: banks are not bound by this law when dealing directly with them for loans). So it is attractive for many so-called brokers to pretend to be independent.

Before meeting with a broker, make sure they have a licence to give you credit (loan) advice. Search the following lists on ASIC Connect’s Professional Registers: Credit Representative, or alternatively they may, in a small amount of cases, hold an ACL (Australian Credit License). Either way, ensure that who you are dealing with is licensed to do so.

So what’s a “caveat loan” and what’s wrong with it?

Caveat loans are private lending agreements between a lender and you, securing a short-term loan against your property. They are quite common in some industries where quick cash is needed and the ability to pay it is evident, thus mitigating potential long-term financing costs. The advantages are:

- Quickly done. There is little underwriting.

- Asset based not income based.

- Money arrives fairly quickly.

The disadvantages:

- Costs/fees. The costs are usually huge. Caveat lenders will rarely get out of bed for less than $30,000 on a deal. Hyped valuation fees, commitment fees and risk fees are the norm.

- Interest rates: The rates usually are about 2-3% per month. This is around 30% per annum rate.

- Credit Protection. Cavet loans are usually made to companies, not to individuals. This allows the lender to make a ‘non-coded’ or non-NCCP loan. This means that as a borrower you are not entitled to any of the protections afforded to you under the NCCP legislation. This is a major piece of legislation and legal defence designed to protect you against bad loans and dodgy lending practices.

For a further chat on anything in the above article, or if you think we can assist, please feel free to reach out and contact us in confidence.

[email protected] or call us for a chat on 07 5456 2928.

We just may be able to help you!

Thanks for reading.