Once legal fees start building, most people hit the same wall:

“How am I actually going to pay for this?”

This is where things often go wrong – not because people make reckless decisions, but because they follow well-meaning but incomplete advice.

After more than 10 years helping clients fund legal matters, I can tell you:

- The biggest financial damage doesn’t come from the case itself

- It comes from the decisions made under pressure

This article covers:

- The biggest trap to avoid (hardship)

- Your real funding options

- What actually works in practice

The Most Common (and Most Dangerous) Advice: “Go on Hardship”

You’ll hear this from:

- Bank staff

- Support workers

- Even people at court

“Just go on hardship – it won’t affect your credit score.”

This is technically true – but completely misleading.

Why Hardship Can Backfire

In my experience of over 10 years helping clients, it almost always backfires.

While it is true that it may not heavily damage your credit score, here’s what actually matters:

- Your ability to borrow

When you enter hardship:

- Lenders see financial distress

- Most will decline you immediately

Even after hardship ends:

- You typically need 6–12 months clean history before a lender will even consider any application.

Think of it from the bank’s point of view – you have admitted to not being able to maintain the payments you previously said, in writing, you would honour.

Now you are looking for even more money without any extra capacity to repay?

Are you serious?!

The Real Impact

During a legal matter, you often need:

- Access to funds

- Flexibility

- The ability to refinance or restructure

If you’re in hardship:

❌ You lose options

❌ You lose leverage

❌ You can get stuck financially mid-case

The Bottom Line on Hardship

- Sometimes necessary

- But rarely strategic

- Do not enter hardship without speaking to a lending expert first.

This is where we come in

Your Real Funding Options

Let’s break down what actually exists – not the theory, but what works in practice.

- Personal Loans (Most Common)

- No property required

- Based on income (PAYG, self-employed, sometimes Centrelink)

- Quick access – can have money within approx. 48 hours

- You control the funds

Best for:

- Early-stage matters

- Moderate legal costs

- Equity Release (No Income Required)

Some lenders offer equity-based lending without traditional income checks.

Example: Plenti used to operate in this space, though products can be inconsistent and difficult to navigate.

Important:

- These are expensive options

- Structures vary widely

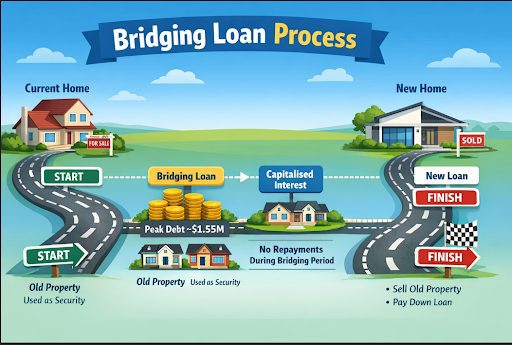

- Solicitor Funding (Caveat Loans)

- Caveat placed on property

- Interest capitalised

- Repaid from settlement

Typical loan: $40k – $80k

Pros:

- No repayments during proceedings

Cons:

- Funds restricted to legal fees

- You’re tied to the lawyer

- Hard to change representation

- Mortgage Equity Release (Traditional)

In theory:

- Refinance and release equity

In reality:

- Often not possible unless both parties cooperate

- Structured Equity Release (Best Case Scenario)

If both parties agree:

- Equity released (up to ~80%)

- Interest can be capitalised

- Clear 6–12 month exit strategy

This is often the cleanest solution:

- Funds legal costs

- Supports separation

- Reduces financial pressure

What Actually Works (After 10+ Years in This Space)

The clients who navigate this best:

- Seek advice early

- Avoid locking themselves into bad structures

- Maintain flexibility wherever possible

The ones who struggle:

- Wait until they’re desperate

- Take advice from non-lending professionals

- Enter hardship too early

Final Thought: This Is a Financial Strategy Problem

Legal matters are emotional. But funding them is not. Ultimately, it is a strategy problem.

And like any strategy:

- The earlier you plan, the more options you keep

If You’re in (or Heading Into) a Legal Matter

Before you:

- Go into hardship

- Commit to a funding structure

- Or run out of cash

Speak to a lending expert (like me) who has done this before. I have been down this road both professionally and personally.

I’ve spent over a decade helping clients fund legal matters, particularly in high-pressure family law situations.

And the truth is simple:

The goal isn’t just to get through court.

- It’s to come out the other side financially intact.