Before diving into why banks have stepped away from bridging finance, it’s worth first understanding what a bridging loan actually is – and when it’s used.

What Is a Bridging Loan?

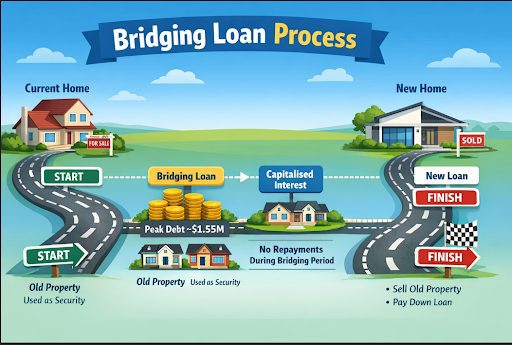

A bridging loan is a short-term loan that allows you to buy a new property before selling your existing one.

Instead of being forced to sell first (often under pressure), a bridging loan “bridges the gap” between the purchase of your new property and the sale of your current one.

During this period, your total debt temporarily increases – known as peak debt – because it includes:

- your existing mortgage

- the new purchase loan

- plus any capitalised interest

Traditionally you had you make repayments on both loans (usually just interest only) during this bridging period. This often causes problems as not everyone earns enough to be able to afford paying for two mortgages at once.

When Are Bridging Loans Typically Used?

Bridging loans can be incredibly useful in a range of real-life situations:

- Moving home – Buy your next property without rushing the sale of your current one

- Downsizing – Take time to achieve the best possible sale price

- Divorce or separation – Access equity quickly to secure a new home

- Buying in a slow or uncertain market – Avoid discounting your property just to meet timelines

- Purchasing before a settlement is complete – where the settlement timing doesn’t line up

- When servicing or cash flow is tight, but equity is strong

- When you’re not confident your bank is giving you all available options

In all of these scenarios, the key benefits are the same: time, flexibility, and control.

Why Banks Don’t Like Bridging Loans

It’s one of the great ironies of modern lending: at a time when Australians arguably need bridging finance more than ever, the major banks have largely stepped away from offering it.

On the surface, this seems strange. But from a bank’s perspective, the decision makes perfect sense.

The Problem with “Peak Debt”

As mentioned, bridging loans create a temporary period of peak debt – often much higher than the borrower’s long-term loan position.

From a bank’s risk perspective, this is a problem.

The loan size increases significantly… but only for a short period.

Once the existing property is sold, the loan is paid down or cleared entirely. This means the bank goes through the effort of assessing, approving, and funding a large loan – only for it to disappear within months.

In simple terms: it’s not profitable.

Low Profit, High Effort

Bridging loans are also operationally inefficient.

Unlike standard home loans, they:

- require manual assessment

- involve complex scenarios (multiple properties, sale assumptions, timing risks)

- often fall outside automated credit systems

There’s no “throughput” efficiency – the kind banks rely on for scale.

So, banks face a poor equation:

-

- More work

- + Higher complexity

- + Lower profitability

Unsurprisingly, most of the majors have exited the space. Those that remain often restrict bridging loans to existing customers only, and even then, with limited appetite.

We’ve seen this before.

The SMSF (Self Managed Super Fund) Lending ParallelA similar pattern played out with SMSF lending several years ago. The major banks withdrew en masse, citing risk and complexity. What followed was the rise of specialist lenders who focused solely on that niche.Bridging finance is now following the same trajectory. |

Why Bridging Loans Matter More Than Ever

Here’s the irony: today’s property market arguably makes bridging loans more valuable than ever.

With:

- economic uncertainty

- fluctuating house prices

- changing government incentives

- and an ageing population downsizing

…the property market is no longer a “done and dusted” process.

Ask any good real estate agent.

Sellers today often face:

- unrealistic expectations

- pressure to accept early offers

- fear-driven decisions

Too many people sell under pressure – only to watch their very same property resold only months later for a far higher price.

A Real Example

Joe and Freda Walsh (names changed for privacy reasons) owned a property in Wollongong, they believed it was worth $1.75 million, but in the current market of uncertainty, agents were pushing them to accept any offers over $1.5 million.

They wanted to move to QLD and buy a $1.1 million property in the Gold Coast – but didn’t want to sacrifice $250,000 just to move quickly.

A bridging solution allowed them to:

- purchase the new property

- retain their existing home until the right price came along

- avoid repayments during the bridging period (interest was capitalised)

Their peak debt was approximately $1.142 million, with six months of interest (~$45,680) added to the loan.

Six months later?…

They sold for $1.75 million – $100,000 above their minimum price and $250,000 more than the original offer.

The bridging loan was repaid in full upon settlement.

Why Specialist Lenders Are Stepping In

Specialist lenders – such as Bridgit, Horizon Finance, Funding.com.au – are now filling the gap left by the banks.

These lenders understand the nature of bridging:

- the loan is short-term by design

- repayment comes from asset sale, not income

- flexibility matters more than rigid servicing models

In many cases:

- no ongoing repayments are required i.e. because interest is added to the loan, there is no regular monthly “out of pocket” repayment.

- income verification may be minimal or unnecessary

- credit issues are less relevant

The focus is on equity and exit strategy, not traditional servicing.

Another Common Scenario: Divorce

Consider a client going through a separation.

One recent case involved a woman who needed to:

- access equity from the former family home

- purchase a new property

- and carry a modest residual loan of $300,000

A bridging solution allowed her to move forward immediately, without waiting for a drawn-out property settlement. The remaining debt was comfortably serviceable on her post-divorce income.

Without bridging finance, she would have been stuck – financially and no doubt emotionally.

A Word of Caution

Not all bridging loans are created equal.

Some “private lenders” operate outside consumer protections, offering:

- extremely high interest rates

- excessive fees (sometimes $50,000+)

- company-structured loans to avoid regulation

This is where regulation matters.

Bridging loans that comply with the National Consumer Credit Protection Act (NCCP) ensure:

- transparent fees

- fair and reasonable interest rates

- responsible lending obligations

- and crucially, the ability for you as a consumer to seek redress if something goes wrong or you feel you’ve been treated unfairly

By contrast, many “caveat loans” are written in company names specifically to bypass these protections – making it extremely difficult (and often impossible) to challenge the lender or seek compensation if you’ve been ripped off.

This is a critical difference – and one which more borrowers should understand before signing anything.

Final Thoughts

Bridging loans are complex – but they solve real problems.

The banks have stepped back because the model doesn’t suit their systems or profitability targets. But for borrowers, the need hasn’t gone away.

In fact, it’s growing.

At Australian Mortgage Corporation, we have the expertise to guide you through these scenarios – ensuring you are not rushed, not pressured, and not forced into decisions that could cost you hundreds of thousands of dollars.

Because sometimes, the ability to wait… is the most valuable financial tool of all.

To discuss a Bridging loan or other lending strategy, since every scenario is different, don’t hesitate to reach out, contact our office, and ask for me personally. Gordon Kelly (07) 5456 2928 or click here to book in for an obligation free chat